Economy

Deflating the Bubble Has Been The Federal Reserve Stronghold Position

Dec

The Fed’s fight against high inflation has not been very successful. During the pandemic, the government has tried to mitigate real estate losses by deflating the bubble and thus preventing another 2007 meltdown.

After the cryptocurrency market was valued at $3 trillion, it has shrunk by more than 2 thirds.

- Technology stocks have fallen more than 50%

- House prices falling for the first time in 10 years

- Surprisingly, all this is happening without affecting the financial system.

Harvard University professor Jeremy Stein, former Federal Reserve Governor from 2012 to 2014, said that “It’s amazing,” “If you had said to any of us a year ago, ‘We’re going to have a lot of 75 hikes. basis points, you would have said, ‘Are you crazy? You are going to blow up the financial system.’”

Bubbles Are Bursting But Not Making a Mess

| Sector | What’s happening | Could be worse? |

|---|---|---|

| Housing | Prices are falling for the first time in 10 years. | Banks are better capitalized and credit standards aren’t as loose as during the 2000s housing bubble. |

| Crypto | Market, once valued at $3 trillion, has shrunk by more than two-thirds. | It’s proved to be largely a self-enclosed ecosystem with the firms inside it mostly indebted to each other. |

| Tech stocks | Investor-favored shares have tumbled more than 50%. | The drop has been gradual and not as steep as the bursting of the dot-com bubble in 2000. |

The Federal Reserve has long refused to use monetary policy to address asset bubbles, fearing that raising interest rates is too blunt a tool for such a mission.

Buy 5 years of premium unlimited access to The WSJ for $69

It is normal that there is a fear of a financial market explosion because of the background of 2007 to 2009, but today there is a stark contrast with the bursting of the US property price bubble at that time.

The Federal Reserve Chairman acknowledges that they have already raised interest rates a lot in a short time, so they are prepared to raise rates to 50 basis points after 4 75 basis point hikes.

+ Here’s how his campaign has helped affect asset markets so far:

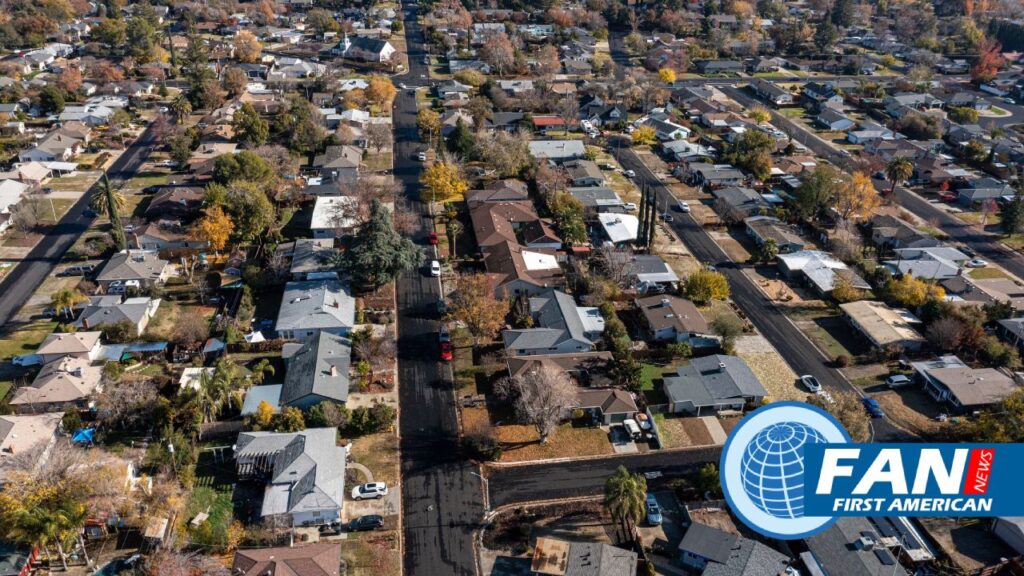

+Cooling of the house, not melting

House prices have skyrocketed on low borrowing costs, coupled with an increase in demand for properties outside urban centers due to the pandemic. With mortgage rates more than doubling this year, prices are falling.

Reforms followed in the aftermath of the financial crisis helped ensure that the latest housing cycle did not feature the kinds of easing in credit standards seen at the turn of the century.

Get full access to the Economist and The Wall Street Journal Digital for $89

The Wrightson economist said there are a lot of deposits in banks, from Americans, who had a lot of savings during the pandemic.

Eliza Winger and Anna Wong wrote for Bloomberg “This housing recession is different from the crash of 2008”, “Mortgage credit quality is higher than it was then”.

Today, shadow lenders are the source of home credit in the US Fannie Mae and Freddie Mac continue to act as effective backers in the mortgage market.

Former Fed official Vincent Reinhart said that “Perhaps we shouldn’t be surprised that housing isn’t more disruptive to the financial system, because we federalized it.”

+Cryptographic collapse, content

Cryptocurrencies have shown to be largely an ecosystem closed in on itself, with the companies within it mostly indebted to one another. More extensive integration with the financial system could have made the recession much more destabilizing.

Brandeis, Stephen Cecchetti compared the cryptocurrency market to a multiplayer online video game. He said that “I was not providing any service to the traditional financial system or to the real economy.”

There are players in the market who were affected by the crypto crash, but the consequences have been minimal elsewhere.

+Tech Tumble, but not Dot-Com Bust

The decline in tech stocks has spread over the past year as Fed rates have risen, ending the healthy levels they reached during the pandemic.

As an example, the Nasdaq is down just over 30% from its 2021 high, but compared to the turn-of-the-century drop of nearly 80% it’s a fraction.

Taking the S&P 500 Index as an example, around 18% below its all-time high reached in January, we can say that the stock market in general has held up even better.

Cecchetti said “In general, stocks are not leveraged,” “And the people who own them tend to be pretty well off.”

+Not all clear

Through so-called quantitative tightening, the central bank continues to reduce its balance sheet and there are rate hikes, although the consequences of the Fed’s anti-inflation crusade are not yet apparent. After bouts of market volatility, the Fed ended the QT process.

The recent explosion in the UK bond market showed that shocks can happen suddenly, which calls for caution. And the Fed does not have the data it should know what is happening in the less regulated shadow banking arena.

The $23.7 trillion US Treasury market was long thought to be the most liquid and stable in the world. Paradoxically, the Dodd-Frank-inspired rules have made the market more fragile by discouraging big banks from acting as intermediaries in buying and selling Treasury securities.

Harvard’s Stein said he shouldn’t take too much comfort in the relative calm so far.

Get 2 Years of The Wall Street Journal Print Subscription with daily delivery for $480

Lindsey Piegza, an economist at Stifel Financial Corp, said while the Fed could “soften” its efforts to tighten credit if faced with major financial disruption, such action would likely be temporary. She also said that “The Fed is very focused on fighting inflation.”

Alan Blinder, a former vice chairman of the Federal Reserve, is among those optimistic that the United States will get through the current cycle without undue financial carnage. He also said, while policymakers always have to worry about what they don’t know, especially unknown unknowns, “I’m reasonably optimistic” a crash can be avoided.

WSJ Digital Edition

The Wall Street Journal Digital Subscription for 1 Year at 70% Off

Barron's Print Edition

Barron's Print Edition

The Economist Digital Edition

NYT Digital Edition

Barron's Digital Edition

Barron’s Newspaper and Washington Post Subscription for 2 Years

Washington Post Digital Edition

The Economist Digital Edition

Wall Street Journal Digital and The Economist 2-Year Combo Package