May

Do we have a banking crisis? – Officials from the Federal Reserve are expected to raise interest rates once more during their upcoming meeting, while also considering whether this will suffice to temporarily halt the most rapid cycle of rate increases witnessed in the past four decades.

“On April 20, Loretta Mester, President of the Federal Reserve Bank of Cleveland, stated that we are significantly nearer to the conclusion of the process of monetary policy tightening than to its initiation.”

The extent of the Federal Reserve’s proximity to that endgame will be a subject of internal discourse, as officials recognize that their messaging regarding forthcoming policy measures can be equally vital to singular adjustments in interest rates.

As they delicately refine their meticulously crafted signals in the post-meeting statement and during Fed Chair Jerome Powell’s press conference on Wednesday following the meeting’s conclusion, officials will probably maintain flexibility and avoid making firm commitments.

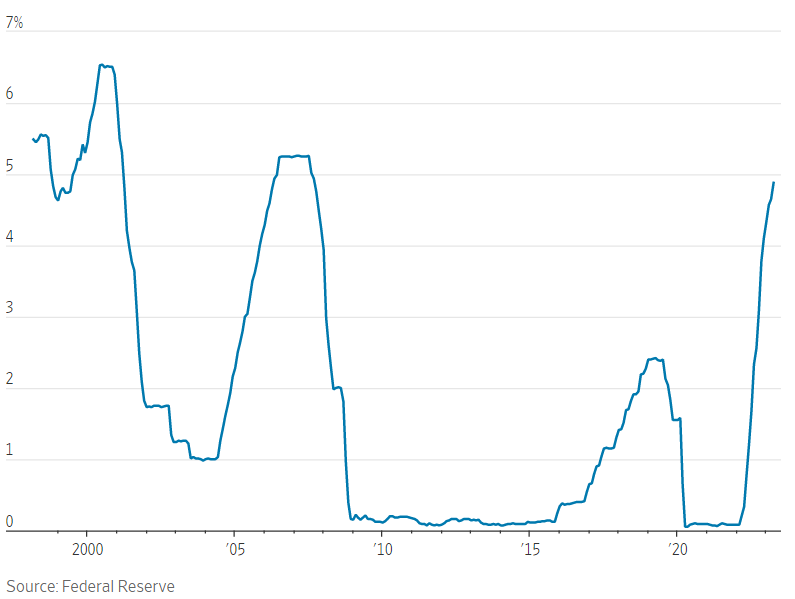

Cumulative change in federal funds rate since start of initial rate increase

If the Federal Reserve were to implement another quarter-percentage point increase, it would raise the benchmark federal-funds rate to a level not seen in 16 years. Since March 2022, the Fed has been gradually increasing rates from nearly zero.

In March 22, Federal Reserve officials raised interest rates by a quarter point to a range of 4.75% to 5%. This increase came at a time when officials had only just begun to confront the potential consequences of two bank failures of moderate size that occurred in the same month.

The recent announcement of the Federal Deposit Insurance Corp’s sale of First Republic Bank to JPMorgan Chase & Co., made public early on Monday, serves as another indication of how banking pressures are casting a shadow over the economic forecast.

Before the upcoming decision on Wednesday, Federal Reserve officials are expected to monitor the investors’ response to the First Republic Bank sale, much like they did before their rate hike six weeks ago. At that time, Swiss regulators merged investment banks UBS Group AG and Credit Suisse Group AG, which also attracted the Fed’s attention.

Though analysts speculate that Monday’s transaction could alleviate some banking pressures, if unexpected and significant financial strains arise before the meeting, officials may need to reconsider their intended rate hike.

To combat inflation, the Federal Reserve utilizes higher interest rates to decelerate the economy. This leads to more stringent financial conditions, including increased borrowing expenses, decreased stock prices, and a strengthened dollar, all of which work to suppress demand.

To date, officials have been searching for distinct indications of a deceleration in economic growth and a decrease in inflation in order to warrant a cessation of rate hikes.

Subscribe today and get 52 weeks of The WSJ Print Edition with daily delivery to your home

However, after this week, the Federal Reserve’s assessment may alter. Officials may require evidence of stronger-than-anticipated expansion, employment, and inflation to persist with the implementation of rate hikes.

The economy has exhibited certain indications of moderation, such as subdued factory activity and consumer spending. Nonetheless, constant employment and substantial wage increases may maintain heightened levels of inflation.

In forecasts released after the March meeting, most Federal Reserve officials believed that the central bank would be required to implement a final quarter-point rate hike before halting their efforts. If officials follow through with their plans this week, they may determine that they have attained a sufficiently stringent environment.

Certain officials have already stated that they intend to observe how the economy progresses throughout the summer before deciding whether it is probable that further rate hikes will be necessary.

In a presentation on April 11, Philadelphia Fed President Patrick Harker stated, “I fail to see why we would simply continue increasing rates in a consistent manner, only to eventually falter and then abruptly decrease rates.” Harker has predicted for some time that the Federal Reserve would be required to implement rate hikes to slightly exceed 5%.

Thus far, officials have limited proof that the banking upheaval in March resulted in a substantial decline in lending, which impacted economic performance. The Fed’s senior loan officer survey, a quarterly evaluation of bank lending trends, will be at the disposal of policymakers during their meeting this week, although it will not be published publicly until after the central bank’s gathering.

The Benchmark federal funds rate

Officials who are more apprehensive about the repercussions of credit conditions becoming tighter are expected to advocate for an indication that the Federal Reserve will halt its rate hikes.

According to Chicago Fed President Austan Goolsbee, while the Fed shouldn’t abandon its efforts to combat inflation, it must also acknowledge that this approach could have distinct effects on certain sectors or regions when combined with other factors.

Eric Rosengren, who served as Boston Fed president from 2007 to 2021, stated last week that if he were still a policymaker, he would vote against a rate increase at this meeting. At an event hosted by Harvard Business School, he expressed the belief that banking stress would have a more detrimental effect on the economy than most Fed officials anticipate.

Meanwhile, a significant number of Fed officials in March expressed the view that if the economic outlook did not deteriorate, more than one rate hike would be warranted this year.

Those officials are more worried that the Federal Reserve might prematurely ease its tightening policy and eventually realize that inflation, hiring, and economic growth are not slowing down as anticipated.

In an April speech, Fed governor Christopher Waller expressed his views stating that until he observes signs of moderating demand and sees inflation moving substantially and continuously towards the 2% target, he would welcome them. However, he believes there is still work to be done.

According to Ray Farris, chief economist at Credit Suisse, while many economists have been concerned about a possible recession, the bigger concern for the Fed is still an economy that is growing too quickly. “Deep down, they wouldn’t mind seeing some genuine economic weakness,” he stated.

Get 2 Years of The Wall Street Journal Print Subscription with daily delivery 6 days a week.

The bottom line is that the Fed’s statement on policy, which will be voted on by the committee, may be the most critical and extensively debated move made by officials this week. At the very least, the central bank is expected to retain a tendency to raise rates rather than indicating a definite pause, similar to the Bank of Canada, which announced its last rate hike in January.

Experts suggested that it would not be beneficial for the Fed to either definitely exclude or suggest a potential rate increase in June. The central bank’s policy statement has contained a commitment to rate hikes at each subsequent meeting since the start of last year, using language that is occasionally known as forward guidance.

“Sometimes, there are situations where the need for forward guidance is not so apparent,” stated John Williams, President of the New York Fed, in a press briefing on April 20.

Adjusting the phrasing of the statement is crucial, as policymakers aim to avoid triggering a market rally that could lead to an early relaxation of financial conditions.

Currently, bond investors predict that the Fed will lower interest rates later in the year. Nevertheless, central bank officials have generally indicated that they plan to keep interest rates unchanged to provide additional constraints on economic growth.

Do we have banking crisis? Read more at WSJ Print Subscription

Vincent Reinhart, Dreyfus and Mellon’s chief economist, explained that since October, investors have been exaggerating any positive news. If the Fed’s messaging becomes “too dovish,” market participants may overreact and push financial conditions too far.

Vincent Reinhart, who provided guidance to Fed officials during the endgame to rate increases in 2006, believes they will seek to steer clear of indicating a rate hike in June. “Committing to one more tightening and then not delivering is a bigger incentive [for markets] to rally,” he said.

In case the policy statement is unremarkable, traders will analyze each expression used by Mr. Powell during his press conference on Wednesday for additional hints. “He’s in a difficult situation because he’s the only thing that stands between investors and a major dovish rally that undermines any policy constraint,” Mr. Reinhart commented.